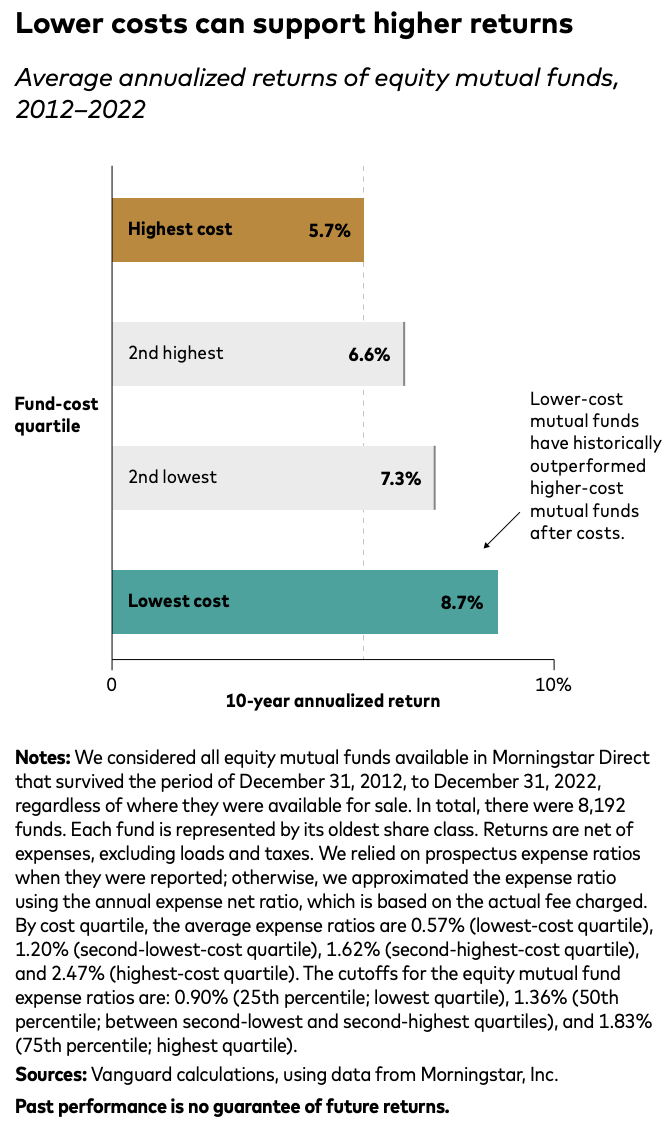

When it comes to investing, your investment strategy costs cut into your returns over the long run. In fact, research from Vanguard found that the cost of an investment is the single best predictor of its future performance. It shouldn't be the only item you evaluate when deciding what to invest in, but can be a good way to compare similar funds.

The main cost you’ll see inside an ETF is the expense ratio. This is the percentage you pay each year to own that investment. Importantly, this does NOT include any fees your financial advisor may charge separately.

The main costs you'll see inside a mutual fund are a sales load (commission) and ongoing 12b-1 marketing fees (buried inside the expense ratio that is an ongoing annual fee, usually up to 1% if the invested amount). Importantly, these do NOT include any fees your financial advisor may charge separately (like Assets Under Management fees, flat fees, or commissions).

ETFs. Why? They usually offer better flexibility, tax efficiency and have lower costs. However, sometimes there may only be mutual fund options such as in many 401(k) plans.

These fees might sound small, but they compound over time. Paying even 1% more each year can mean tens of thousands of dollars lost from your portfolio over decades.

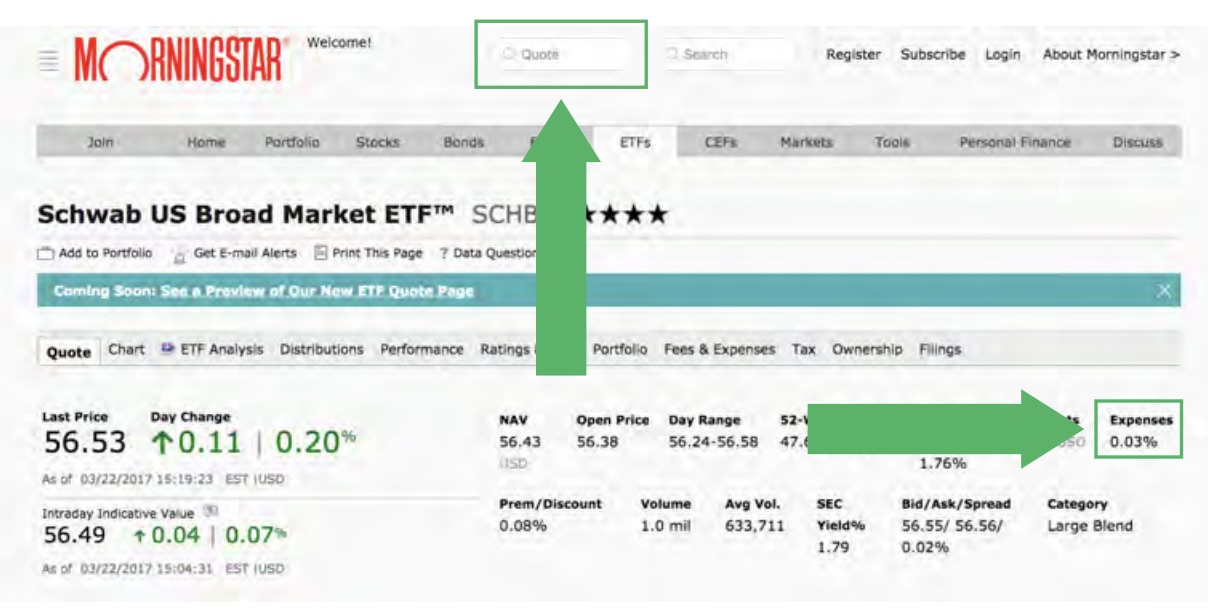

When reviewing your accounts, ask your financial advisor (or yourself if you DIY investments) about the expense ratios of the funds you're invested in. If you have ticker symbols, you can plug them into Morningstar and see the expense ratios right away (see image below). Knowing what you’re paying is one of the first steps to making smarter investment decisions.

1. Lower-cost investments have historically outperformed higher-cost alternatives.

2. The less you pay in investment costs, the more of your returns you keep.

3. You can't control the ups and downs of the market, but you can control what you pay in fees and taxes.

Say you need $500 to fix a flat tire so you can get to work. You know you’re getting paid soon, but don’t have the money now. You go to the nearest payday loan store to borrow the money.

According to the Consumer Financial Protection Bureau, the average payday lender will charge $15 in fees for every $100 borrowed. For a $500 loan repaid in two weeks, that’s $75 total in fees — which equates to an APR of around 400%!

Why is it so high? A few reasons:

The good news is entrepreneurs and financial innovators are working on ways to provide fairer, lower-cost liquidity options for people who need short-term access to cash.

You can turn all your dreams into reality. Find your passion, chase after it, and change the world. Hook ‘em” - Kendra Scott

Ready to Take Off?

📩 Have a financial question? Visit The Financial Takeoff and our Ask a Question page.

🚀 Want to explore working together? Schedule your Initial Collaboration meeting to see what’s possible with your financial planning. We look forward to meeting you!

Life is short and time is precious. Thanks for taking yours to read this and I hope to be a part of your Financial Takeoff!

Disclaimer: This is just for informational purposes and should not be used or viewed as tax, legal, or financial advice. Work with your tax professional, legal professional, and financial planner to evaluate which strategies would be the best for your situation.